Table of Contents

- What is an embedded payment?

- What are the benefits of embedded payments?

- How do embedded payments work?

- How do embedded payments impact b2b purchases?

- What is the future of embedded finance?

Key Takeaways

- Embedded payments streamline business transactions by integrating payment processes directly into platforms, reducing friction in invoicing, reconciliation, and cash flow management.

- This technology allows customers to complete purchases within apps or websites, enhancing convenience and potentially increasing conversion rates.

- Embedded payments improve security with tokenization and encryption, protecting sensitive financial information.

- In B2B contexts, embedded payments can boost cash flow and reduce Days Sales Outstanding, improving financial performance.

Embedded payments are revolutionizing how businesses transact, eliminating the friction traditionally associated with invoicing, reconciliation, and cash flow management. By enabling digital payments directly within a company’s platform, this technology reshapes the entire payment experience, from ACH payments to complex, multi-channel invoicing processes. They streamline every step, creating a more convenient and secure way for businesses to manage transactions.

Are you curious to see how this transformative payment technology works and how it can benefit your business? Dive deeper to explore how embedded payments drive efficiency, enhance security, and reshape B2B digital payments.

What is an Embedded Payment?

An embedded payment method lets customers purchase directly from a mobile app or website without leaving the platform. This makes it easier and more convenient for customers to make purchases, as they don't have to switch between different apps or websites to complete their transactions.

Embedded payments are typically processed through a third-party payment processor like Stripe or PayPal. This allows businesses to accept payments from various sources, including credit cards, debit cards, and e-wallets.

Some companies have taken this further into what is known as embedded banking, a fintech segment that includes a range of financial services that can be provided by businesses that are not banks or financial institutions. Here, interactions with a formal bank account can be made without requiring the customer to log into an account from the bank’s app or website.

To implement embedded payments, businesses need to:

-

Choose a payment processor: There are many different payment processors, each with fees and features. Businesses should choose a payment processor that fits their needs and budget.

-

Integrate the payment processor with their platform: Once a payment processor has been chosen, businesses must integrate it. This typically involves adding a few lines of code to the platform's checkout page.

-

Test the payment process: Once the payment processor has been integrated, businesses should test it to ensure it works properly.

What Is an Embedded Payment Example?

There are many different ways to use embedded payments:

- E-commerce websites with ‘Pay-Now’ clickable buttons allow customers to checkout directly, enhancing conversion rates.

- Mobile apps offer embedded payments and digital wallets for convenient in-app purchases.

- Social media platforms can use embedded payments for direct product purchases, benefiting businesses by expanding customer reach and boosting sales.

- Point-of-sale (POS) systems facilitate payments at the point of sale, eliminating the need for cash or credit cards.

What Are the Benefits of Embedded Payments?

Embedded payments have numerous benefits for businesses and consumers alike. Here are some key advantages:

- Seamlessness and convenience: By streamlining purchases, embedded payments improve user satisfaction, reducing cart abandonment.

- Increased conversion rates: Streamlined checkout processes make it easier for customers to complete purchases, leading to higher conversion rates and increased revenue.

- Improved security: Advanced security measures, like tokenization and encryption, protect sensitive financial data, reducing the risk of fraud and unauthorized transactions.

- Personalized payment options: Embedded payments can integrate customer data and preferences to offer customized payment options, such as preferred payment methods for one-click checkout or tailored financing options.

- Enhanced customer engagement: Offering loyalty programs, rewards, and other incentives can help businesses build stronger customer relationships and increase repeat purchases.

- Streamlined reconciliation: A consolidated view of all transactions can simplify the reconciliation processes, saving time and reducing the risk of errors.

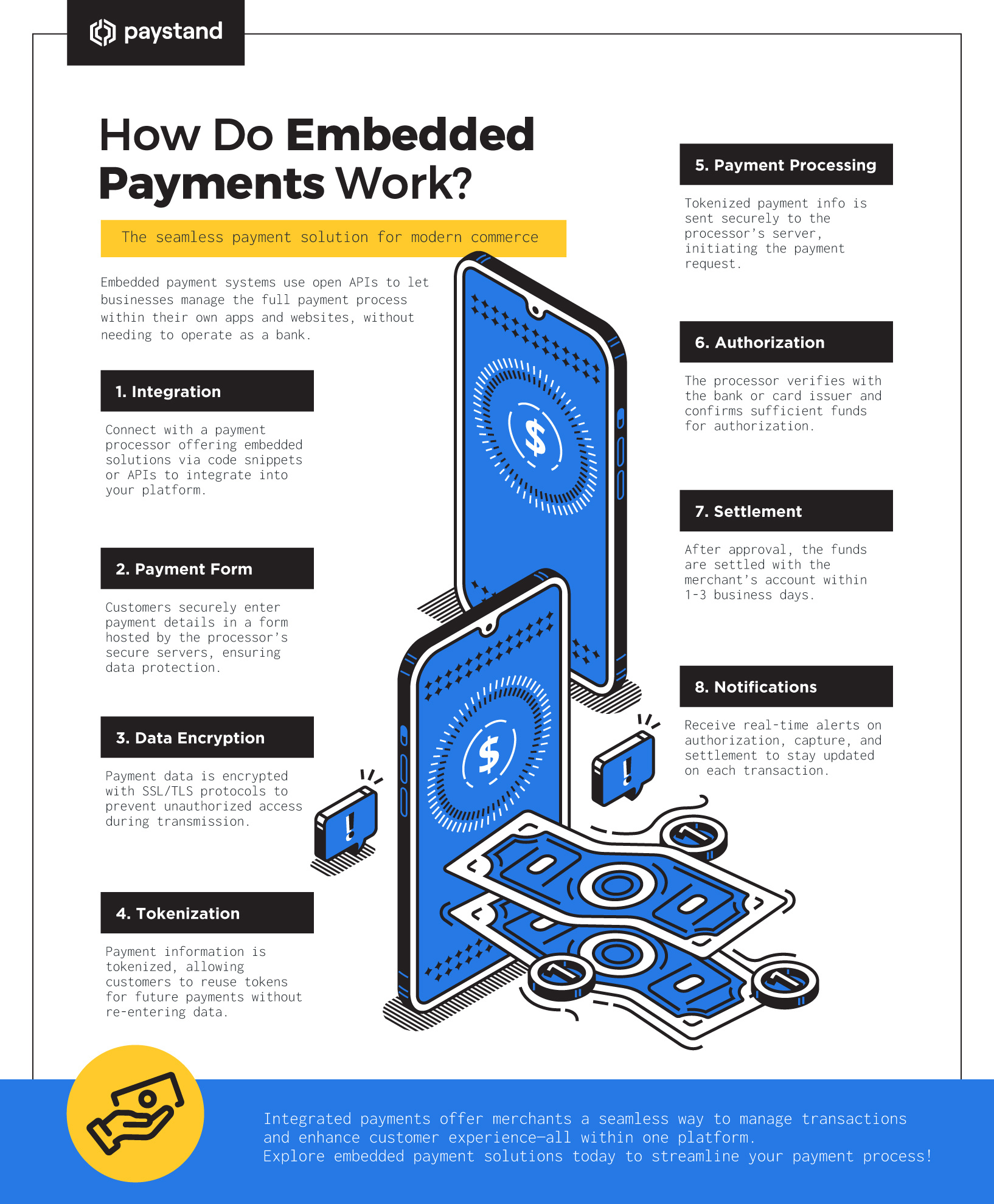

How Do Embedded Payments Work?

Embedded payment systems function through open APIs that embed an upstream payment processing tool within a different app or website. This allows merchants not operating as banks or financial institutions to oversee the payment process from start to finish. The steps to implement embedded payments are the following:

-

Integration: Partner with a payment processor that offers embedded payment solutions, providing code snippets or APIs for integration into your platform.

-

Payment form: Customers can securely enter their payment information on a payment form hosted on the payment processor's secure servers, ensuring the highest level of security.

-

Data encryption: When entered, customer payment information is encrypted using industry-standard encryption protocols like SSL/TLS, preventing unauthorized access to sensitive data during transmission.

-

Tokenization: Payment processors can tokenize customers' payment information by creating unique tokens representing their credentials. These tokens can be used for future transactions, eliminating the need to re-enter payment details every time.

-

Payment processing: When a customer clicks the "Pay" button, the tokenized payment information is securely transmitted to the payment processor's servers for authorization, initiating the payment process.

-

Authorization: After receiving payment information, the payment processor verifies it with the customer's bank or card issuer and checks for sufficient funds. If the authorization is successful, the payment is approved.

-

Settlement: Upon payment authorization, the payment processor settles the funds with the merchant's account, and the funds are typically deposited within one to three business days.

-

Notifications: Receiving real-time notifications about the payment status, including authorization, capture, and settlement, enables you to track transactions and ensure a smooth payment flow.

How Do Embedded Payments Impact B2B Purchases?

Integrating embedded payments offers businesses a convenient and efficient way to accept payments within their existing software platforms. It streamlines the process and eliminates the need for customers to navigate to a separate payment page, enhancing user experience. This simplicity and ease of use encourage customers to make repeat purchases, increasing order volume and purchase frequency for B2B businesses.

Customers' trust in embedded payments drives repeat business and brand loyalty. They feel more comfortable knowing that any payment-related issues will be effectively resolved. This trust in the embedded payment solution fosters positive customer relationships and enhances the overall brand experience.

Embedded payments also significantly benefit AR teams by automating manual processes and reducing DSO. Automating payment processing tasks, such as invoice generation, payment reminders, and reconciliation, frees up valuable time for AR teams, allowing them to focus on strategic initiatives that drive business growth. Additionally, by reducing DSO, embedded payments help businesses improve cash flow and optimize their financial performance.

What is the Future of Embedded Finance?

The future of embedded finance holds immense potential for revolutionizing the way financial services are consumed and integrated into everyday life. Paystand is at the forefront of embedded payment technology, providing businesses with advanced automation and AR optimization tools.

Paystand empowers businesses to speed up collections, reduce manual workload, and optimize financial processes by seamlessly integrating digital payment options like ACH payments into platforms and the Paystand B2B Network. This innovation makes transactions more efficient and boosts cash flow by minimizing delays and lowering DSO.

Want to learn more about how embedded payments can transform your B2B payment processes? Download our ebook The Future of Finance to discover how to make every transaction smoother, faster, and more secure.