Table of Contents

- What Are Digital Payments?

- Types of Digital Payments

- How Are Digital Payments Processed?

- Advantages of Digital Payments

- Digital Payment Platforms

- Traditional Payments vs. Digital Payments

- Are Digital Payments Safe?

- How Do Digital Payments Differ from Checks?

Key Takeaways

- Digital payments streamline AR processes and accelerate collections.

- 40% of B2B payments remain manual despite efficiency gains in digital transactions.

- Digital payment platforms enhance cash flow, security, and ERP integration.

- Paper checks are costly, slow, and the top source of B2B payment fraud.

- Paystand offers an automated B2B payment solution for optimized cashless transactions.

Digital payments boost business growth, but accounting departments are slow to adopt. Switching from paper checks to digital forms of payment accelerates AR processes and collections.

B2B payments are now customer touchpoints. These transactions are no longer back-office tasks; they’re crucial customer touchpoints. A study shows checkout experiences affect repeat business and that cashless payment methods drive fast, efficient growth.

Consumer payments have evolved, and most now occur digitally through payment apps and online platforms. Contactless payment is the present standard in our move towards a cashless society.

Despite advancements, 40% of B2B payments are still manual. The pandemic highlighted the costly inefficiencies of traditional systems.

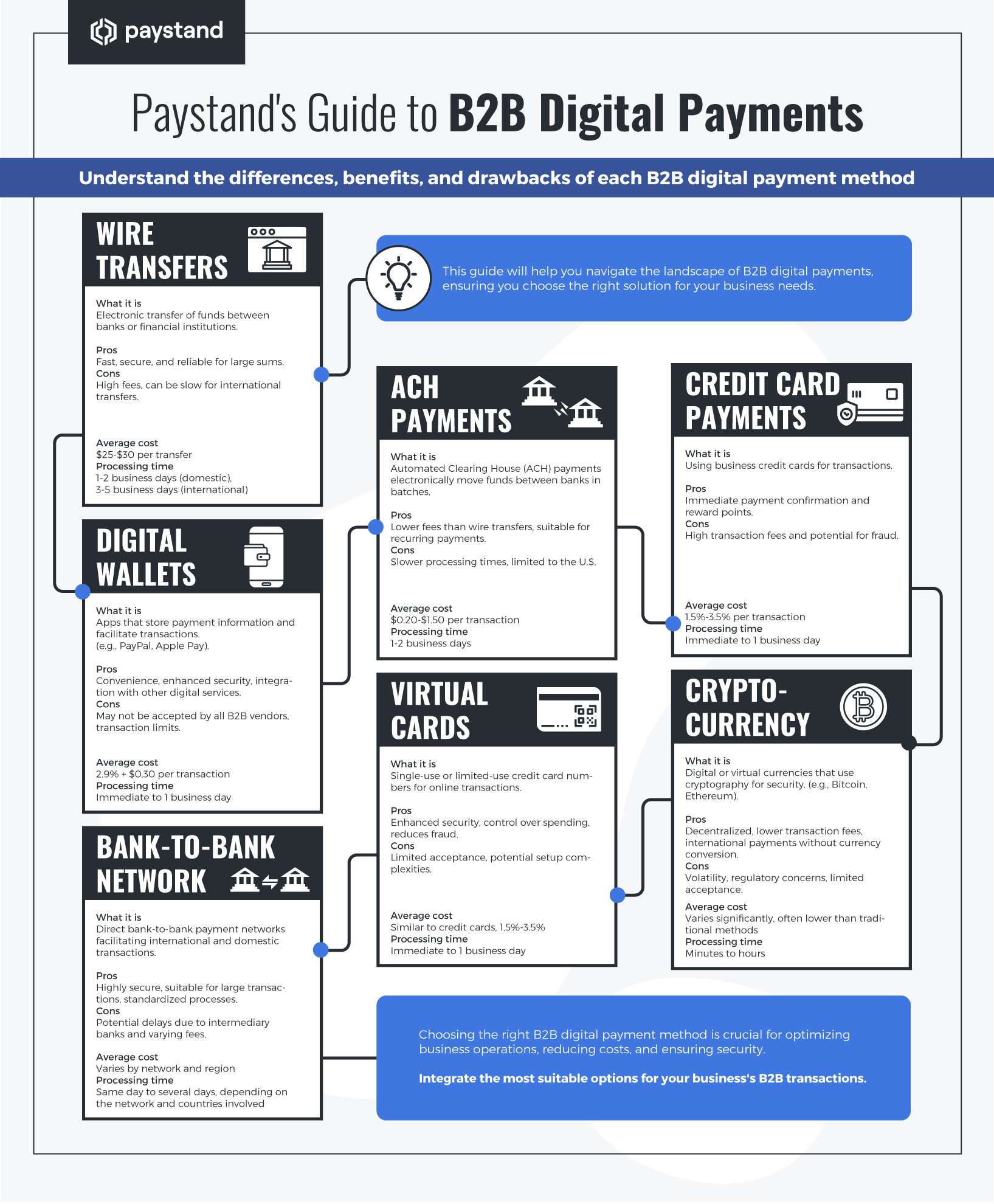

What Are Digital Payments?

Digital payments transfer funds electronically using various methods, such as bank wires, ACH transactions, and mobile payment systems. These methods reduce reliance on paper checks, streamline cash flow, and minimize errors in payment processing.

Types of Digital Payments

Digital payment methods include:

- Mobile payments through apps like Venmo and Zelle.

- Bank wires and ACH transfers for direct transactions.

- QR codes for seamless digital transactions.

- Digital wallets such as Apple Pay and Google Pay.

How Are Digital Payments Processed?

Digital payments follow a streamlined electronic process:

- Payment initiation – The payer selects a payment method and enters payment details.

- Authorization and verification – The payment gateway verifies credentials and ensures sufficient funds.

- Transaction processing – The payment network routes the transaction to the appropriate financial institutions.

- Settlement and reconciliation – Funds are transferred, and transactions are recorded in the system.

Advantages of Digital Payments

Switching to digital payments provides significant business benefits, including:

- Consistent cash flow – Faster payments improve financial stability.

- Time and cost savings – Automates processes and reduces operational costs.

- Enhanced security – Reduces fraud risk through encryption and authentication.

- ERP integration – Seamlessly connects payments to accounting and reconciliation systems.

Digital Payment Platforms

Digital payment platforms allow businesses to process transactions efficiently and securely.

Key Benefits:

- Convenience – Customers can pay online with a single click.

- Security – Advanced encryption protects sensitive data.

- Efficiency – Automates invoicing, payment processing, and reconciliation.

- Cost-effectiveness – Eliminates postage, printing, and manual processing costs.

Paystand’s Features:

- AR Management – Automates accounts receivable for seamless collections.

- Virtual Terminal – Enables card-not-present transactions.

- Payment Portal – Offers self-service and multiple payment options.

- Fund on File – Securely stores payment details for future use.

Traditional Payments vs. Digital Payments

Traditional, paper-based payments are costly, slow, and prone to fraud. Processing a check can cost $4-$20 and take up to 15 days to clear, delaying cash flow and increasing DSO.

Challenges of Traditional Payments:

- Lengthy payment cycles and processing delays.

- Higher fraud risks due to manual handling.

- Insufficient fund issues from stopped payments.

Since 2020, businesses have increasingly adopted digital payments for efficiency and security benefits.

Are Digital Payments Safe?

Contrary to popular belief, digital payments are more secure than checks. The Association for Finance Professionals reports that 73% of B2B fraud attempts involve checks, while digital transactions employ advanced encryption and authentication to prevent tampering.

Security Features:

- Encryption and tokenization – Protects payment data.

- Smart contracts and algorithms – Automate compliance and validation.

- Minimal handling – Reduces fraud exposure compared to checks.

How Do Digital Payments Differ from Checks?

| Feature | Digital Payments | Checks |

|---|---|---|

| Processing Time | Instant to 1-2 days | 5-15 days |

| Security | High (encryption, fraud detection) | Low (susceptible to tampering) |

| Cost Efficiency | Low transaction fees | $4-$20 per check |

| Automation | Fully automated | Manual processing |

| Fraud Risk | Low | High (73% of fraud cases) |

Elevate Your AR with Paystand

Paystand provides a fully automated B2B payment solution, reducing transaction costs and increasing efficiency.

Ready to streamline your cashless transactions? Explore our ebook on the competitive advantages of digital payments.

%20(1)%20(1).jpg?width=100&height=100&name=IMG_3752%20(1)%20(1)%20(1).jpg)