Table of Contents

- What Is An Automated Clearing House (ACH) Credit?

- How Do ACH Credits Work?

- What Is The Difference Between ACH Credits And ACH Debits?

- Benefits Of ACH Credits

- Limitations of ACH Credit

- Better Alternatives to ACH Payments for Businesses

Key Takeaways

- ACH credits are electronic payments pushing funds from the payer’s account to the payee’s account.

- ACH credits involve sending funds, while ACH debits pull funds from accounts.

- ACH payments are generally secure, with encryption and anti-fraud measures in place.

- ACH credits need a routing number, account number, and account type for processing.

- Paystand's blockchain-based network offers zero fees, faster processing, and real-time transparency compared to ACH.

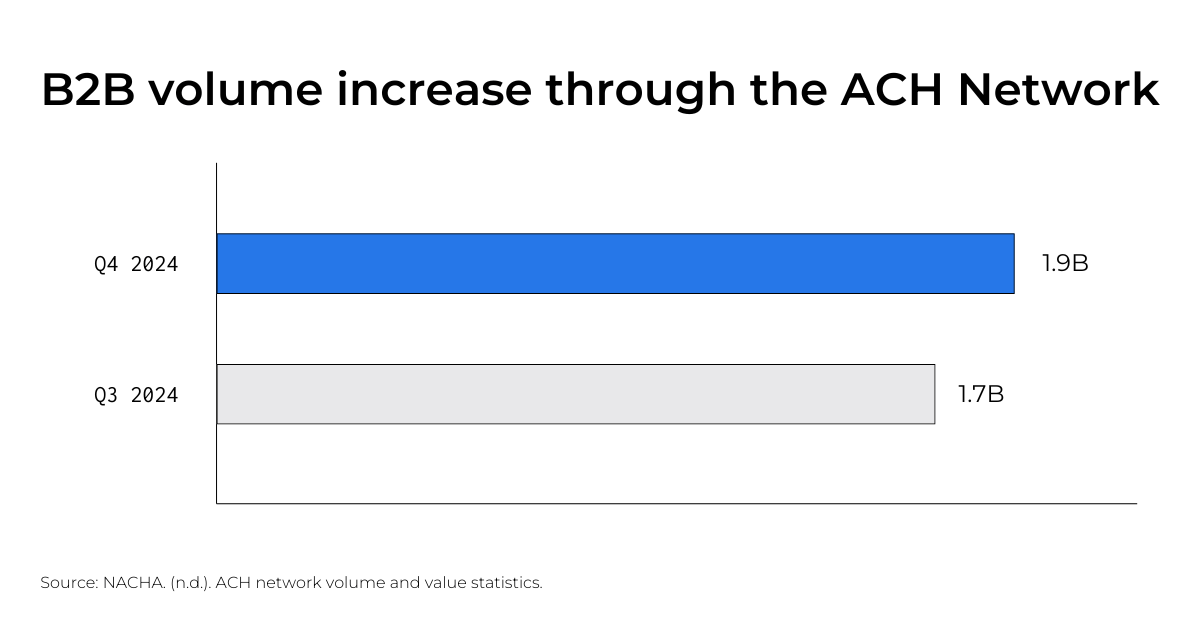

Companies of all sizes have long used the ACH Network to receive and make payments digitally–from payroll deposits and tax refunds to vendor transactions. In the third quarter of 2024 alone, B2B processed 1.9 billion payments through the ACH Network, marking an increase of 12.6% from Q3 2024.

Nevertheless, today’s businesses require payment methods that do not have the limitations of ACH: slow processing times, transaction fees, and a lack of real-time transparency.

What Is An Automated Clearing House (ACH) Credit?

An Automated Clearing House (ACH) credit is a type of ACH transfer in which funds are pushed into a bank account. This means that the sender of the payment triggers the funds to be sent to the receiver of the payment.

ACH stands for Automated Clearing House: the official electronic network that initiates payments from one bank account to another. It connects over 10,000 banks and financial institutions in the US. ACH payments are run by the National Automated Clearing House Association (NACHA) and include different payment categories such as direct deposits, peer-to-peer payments, bill payments initiated by e-commerce platforms, and ACH payments initiated by paper checks.

How Do ACH Credits Work?

An ACH credit transaction streamlines the process of transferring funds electronically. Instead of issuing a physical check, like in the old days, the payer instructs their bank to send money directly to the recipient’s account. Here’s how the process unfolds:

- Initiation: The payer provides payment instructions to their bank or payment provider, including the recipient's banking details.

- Batch Processing: The bank consolidates the transaction with others into a batch and submits it to the ACH Network for processing.

- Clearing and Settlement: The ACH Network processes the batch, ensuring transactions are routed and settled with the appropriate receiving banks.

- Deposit: The receiving bank credits the funds to the recipient's account once the transaction is cleared.

This process generally takes 1-3 business days to complete, but it might be delayed if the transaction is made on weekends or holidays.

ACH Credit Origination

ACH credit origination refers to the process by which an organization or individual initiates an ACH credit transaction. It involves the following steps:

- Authorization: The payer agrees to send funds and provides their banking details.

- Submission: The transaction details, including the recipient's account information, are submitted to the originating bank.

What Is The Difference Between ACH Credits And ACH Debits?

ACH debits (also known as direct payments) differ from ACH credits in one very specific respect: while ACH credits allow funds to be directly deposited from the payer’s account into the payee’s account, ACH debits pull funds from the payer’s account directly and transfer them into the payee’s account.

Benefits Of ACH Credits

The American Payroll Association (APA) conducted a survey in 2022 and revealed that over 93% of survey participants used ACH credits as their chosen payment method. This popularity is greatly due to 4 main benefits: security, cost-effectiveness, wide acceptance, and the ability to perform the transaction without having to meet physically.

Is ACH Safer Than Credit Cards?

ACH payments are generally considered safer than credit card transactions, particularly for B2B payments. Why? There are fewer intermediaries, encrypted ACH transfers, and more robust fraud prevention measures.

While credit cards have advanced security features like tokenization, they are more vulnerable to fraud due to the involvement of multiple intermediaries, including payment processors and card networks.

Limitations of ACH Credit

Despite its benefits, ACH credit has limitations that businesses need to consider:

- Payments can take 1-3 business days, which may not be ideal for time-sensitive transactions.

- While it has lower fees than credit card fees, ACH transactions still incur processing fees.

- There is no real-time tracking, leading to uncertainty about payment status.

Better Alternatives to ACH Payments for Businesses

While ACH payments have been a reliable option for decades, businesses today require faster, more cost-effective, and transparent solutions to meet modern demands. Paystand’s blockchain-based payment infrastructure provides a superior alternative with the following advantages:

- Speed: Paystand uses blockchain technology to enable real-time fund transfers, ensuring payments are quickly processed.

- Cost: Paystand’s B2B Network eliminates transaction fees entirely, ultimately helping companies increase profitability.

- Transparency: The B2B Network, powered by blockchain technology, provides real-time tracking and immutable records.

- Automation: Paystand’s stack automates accounts receivable workflows, minimizing manual processes. Features like recurring billing, automated reminders, and payment reconciliation reduce errors and improve operational efficiency.

Our innovative approach empowers businesses to move beyond the limitations of ACH and credit cards, providing a faster, more cost-effective, and transparent payment solution.

To discover how Paystand can revolutionize your payment processes and improve your financial operations, schedule a demo today.